To help you get familiar with the ISSB and the IFRS Sustainability Disclosure Standards, read:

- an introduction to the ISSB

- an overview of the new IFRS Sustainability Disclosure Standards, IFRS S1 and IFRS S2

- a guide for using IFRS Sustainability Disclosure Standards to disclose decision-useful information

This section gives a brief overview of the International Sustainability Standards Board (ISSB), its purpose and its role in the global reporting landscape.

Today, sustainability-related information—information about the risks and opportunities arising from a company’s interactions with its stakeholders, society, the economy and the natural environment—is increasingly integral to economic and investment decisions. Responding to the demand for such information, the IFRS Foundation created the ISSB.

The purpose of the ISSB is to empower capital market participants with the right information to support better economic and investment decision-making. The ISSB uses a transparent, rigorous due process to develop market-informed standards that:

- enable companies to disclose decision-useful, comparable information; and

- consolidate the ‘alphabet soup’ of voluntary sustainability-reporting initiatives.

The ISSB has consolidated and built on the work of market-led reporting initiatives (as illustrated in the graphic)—comprising the Climate Disclosure Standards Board (CDSB), the Task Force for Climate-related Financial Disclosures (TCFD), the Value Reporting Foundation’s Integrated Reporting Framework and the Sustainability Accounting Standards Board (SASB).

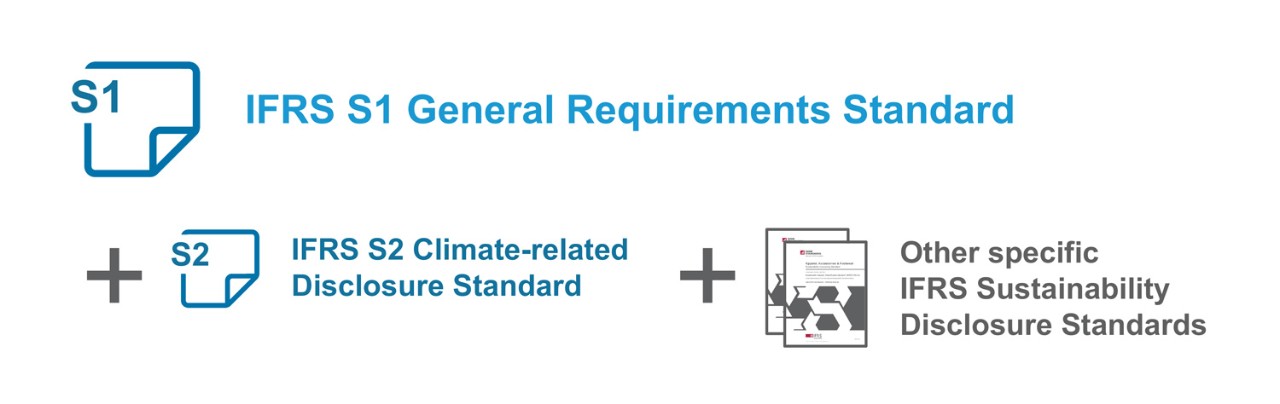

The ISSB issued its inaugural IFRS Sustainability Disclosure Standards—IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information and IFRS S2 Climate-related Disclosures—in June 2023. The ISSB Standards establish a high-quality global baseline of investor-focused sustainability-related disclosures.

- IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information provides a set of disclosure requirements designed to enable companies to communicate to investors about the sustainability-related risks and opportunities they face over the short, medium and long term. The information provided about sustainability-related risks and opportunities is based on the four content elements set out in the TCFD recommendations and in addition, industry-based information is required to be provided.

- IFRS S2 Climate-related Disclosures sets out specific climate-related disclosure requirements for a company to disclose information about its climate-related risks and opportunities. IFRS S2 builds on the requirements set out in IFRS S1 and fully integrates the TCFD recommendations.

The International Organization of Securities Commission (IOSCO) announced its endorsement of the ISSB Standards—encouraging their widespread adoption and sending a strong signal to jurisdictions around the world about its confidence in implementing the ISSB Standards into regulatory frameworks.

The ISSB Standards are suitable for application around the world. Both IFRS S1 and IFRS S2 are available for immediate application.

Watch this three-minute video about IFRS S1

Watch this four-minute video about IFRS S2

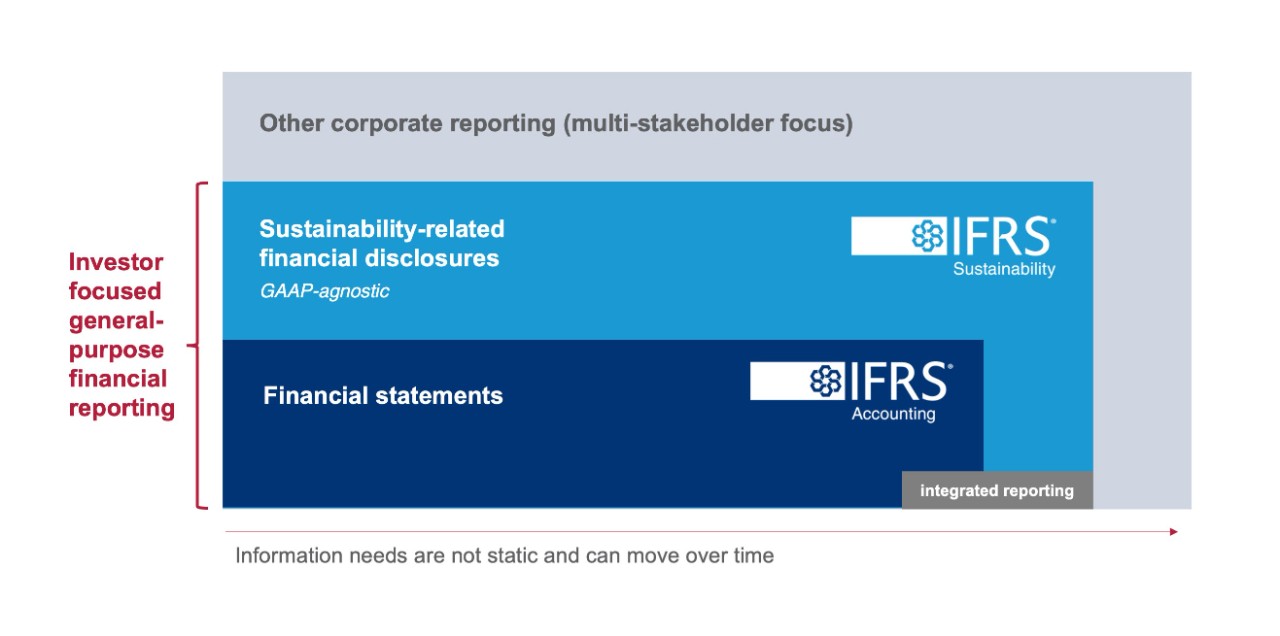

IFRS Standards (both Accounting and Sustainability Disclosure Standards) are designed to meet the needs of existing and potential investors, lenders and other creditors.

The decisions of investors relate to providing resources to a company and can involve decisions about:

- buying, selling or holding equity and debt instruments;

- providing or selling loans and other forms of credit; or

- exercising rights to vote on, or otherwise influence the company’s management’s actions that affect the use of the company’s economic resources.

Investors need consistent, complete, comparable information that can be used to assess a company’s exposure to and management of sustainability-related risks and opportunities over the short, medium and long term. Such information supplements and complements the information in a company’s financial statements.

ISSB Standards enable companies to deliver high-quality and decision-useful information—that can be assured—to investors.

ISSB Standards build upon and consolidate the work of pre-existing initiatives and borrow well-known concepts from standards, therefore streamlining the disclosure process for companies getting started or long-time reporters. Those who have previously used these standards and frameworks are well positioned to apply ISSB Standards.

The ISSB is focused on simplifying the landscape even further by ensuring its standards work well with jurisdictional requirements, when relevant, and with the GRI Standards so that a common baseline of information is available.

Likely benefits for companies applying ISSB Standards include positive effects on governance, business strategy, access to capital, reputation and employee and stakeholder engagement. Applying IFRS S1 and IFRS S2 will help companies streamline their sustainability reporting processes, providing better information to help investors make better investment decisions.

ISSB introduced mechanisms to support application

The ISSB designed many requirements in IFRS S1 and IFRS S2 to be applied in a manner appropriate for a company’s circumstances—that is, the requirements are ‘proportionate’ to the range of capabilities and varied sustainability reporting experience of companies around the world. For example, the instruction in some parts of the standards to use reasonable and supportable information available without undue cost or effort.

The ISSB Standards also include guidance to help companies understand how to apply ISSB Standards and refer to sources of guidance to assist companies in reporting on sustainability-related topics beyond the climate-related disclosures required by IFRS S2. This guidance is discussed further in the later sections.

The ISSB Standards also allow for relief from some requirements, depending on a company’s circumstances. For example, a company might not have the skills, capabilities or resources to provide quantitative information about the anticipated financial effects of a sustainability-related risk or opportunity. If so, the company is permitted to provide qualitative rather than quantitative information.

ISSB Standards provide an opportunity for companies’ disclosures to be globally consistent and comparable across capital markets.

The ISSB has established ISSB Standards to provide a global baseline of information to meet the needs of capital markets. It is working with jurisdictions around the world, as well as market participants, with the objective of having the ISSB Standards used around the world both as a result of regulatory adoption and voluntary use. In an effort to achieve a globally consistent baseline, the ISSB’s Standards are built on or incorporate commonly used standards and frameworks. The table below summarises the relationships with some of these standards and frameworks.

Task Force for Climate-related Financial Disclosures (TCFD)

The IFRS S1 and IFRS S2 core content areas of governance, strategy, risk management, and metrics and targets are consistent with, and build on, TCFD recommendations. Therefore, a company need not apply the TCFD recommendations in addition to the ISSB Standards.

This IFRS S2–TCFD comparison table [updated in November 2024] summarises the minor differences between IFRS S2 and the TCFD recommendations.

SASB Standards (SASB)

IFRS S1 requires a company to consider SASB disclosure topics when identifying industry-specific sustainability-related risks and opportunities. The company is also required to consider SASB metrics when identifying industry-specific information about sustainability risks and opportunities in the absence of a specific ISSB Standard.

IFRS S2 requires a company to consider the accompanying guidance on climate-related disclosure topics and metrics. The IFRS S2 industry-based metrics and disclosure topics have been derived from SASB Standards with amendments to improve international applicability.

Integrated Reporting Framework

IFRS S1 builds on concepts from the Integrated Reporting Framework relating to a company’s ability:

- to generate returns for investors, lenders and other creditors;

- to communicate how it creates value given its dependencies on and interactions with other stakeholders, resources and relationships.

Climate Disclosure Standards Board (CDSB)

When applying IFRS S1 requirements, a company is permitted to consider the CDSB Framework application guidance in the absence of an applicable ISSB Standard. The guidance can be used when identifying sustainability-related risks and opportunities and disclosing information (including metrics) about such sustainability risks and opportunities.

International Accounting Standards Board (IASB)

The International Accounting Standards Board’s (IASB) definition of material information and primary users is consistent with the Conceptual Framework for Financial Reporting (Conceptual Framework).

IFRS S1 uses definitions and requirements that are consistent with the IASB’s Conceptual Framework, IAS 1 Presentation of Financial Statements and IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors.

The characteristics described in Appendix D of IFRS S1 are adapted from the IASB’s Conceptual Framework.

Greenhouse Gas Protocol

IFRS S2 requires companies to measure their scope 1, scope 2 and scope 3 greenhouse gas emissions in accordance with the Greenhouse Gas Protocol: A Corporate Accounting and Reporting Standard (2004). IFRS S2 requires companies to disclose information about their scope 1, scope 2 and scope 3 greenhouse gas emissions. This includes information about which of the 15 categories defined in the GHG Protocol Corporate Value Chain (scope 3) Accounting and Reporting Standard (2011) are included in a company’s emissions measurement.

IFRS S1 and IFRS S2 prescribe how a company prepares and reports its sustainability-related financial disclosures and climate-related disclosures. This section provides an overview of the objectives and disclosures prescribed in the ISSB Standards.

In making decisions about providing resources to a company, investors need information about the company’s sustainability-related risks and opportunities.

IFRS S1 requires a company to decide what constitutes a risk or opportunity in the context of its own facts and circumstances. Companies often have well-established processes for identifying, assessing, and responding to risks and opportunities based on business objectives and risk appetites. IFRS S1 and IFRS S2 include accompanying guidance and refer to other sources of guidance to assist a company in the identification of sustainability-related risks and opportunities. But, it is ultimately up to the company to decide which risks and opportunities it reports.

What sustainability-related risks and opportunities do the ISSB Standards focus on?

The focus of the ISSB Standards is on sustainability-related risks and opportunities that could reasonably be expected to affect the company’s cash flows, its access to finance or the cost of capital over the short, medium or long term (these financial effects are also referred to as a company’s prospects).

IFRS S2 specifically focuses on climate-related risks and climate-related opportunities that are reasonably expected to affect a company’s prospects. Climate-related risks include both physical risks (such as those resulting from increased severity of extreme weather) and transition risks (such as those associated with policy action and changes in technology that can affect how a company can run its business). Climate-related opportunities refer to the potential positive effects arising from climate change for a company.

Sustainability-related risks and opportunities (including climate-related risks and opportunities) that could not reasonably be expected to affect a company’s prospects are outside the scope of IFRS S1 and IFRS S2.

What do sustainability-related risks and opportunities arise from?

Sustainability-related risks and opportunities can be concentrated within the reporting company and throughout its value chain.

Sustainability-related risks and opportunities arise from a company’s interactions with stakeholders, society, the economy and the natural environment. These interactions—specifically impacts and dependencies—occur through a company operating its business model and from the external environment in which the company operates. The company’s exposure to and management of critical dependencies and its impacts can give rise to risks and opportunities that could reasonably be expected to affect the company’s prospects.

Example 1

For example, a company’s business model might depend on a natural resource such as water. The company could both affect, and be affected by, the quality, availability and affordability of that resource. As a result, the degradation or depletion of that resource could create a risk of the company’s operations being disrupted and the company’s business model or strategy being affected. Such disruption could ultimately negatively affect the company’s financial performance and financial position. But the regeneration and preservation of that resource could positively affect the company.

Example 2

Take, as another example, a company that operates in a highly competitive market and requires a highly specialised workforce to achieve its strategic purposes. The company’s future success will likely depend on its ability to attract and retain that resource. That ability will depend, in part, on the company’s employment practices—such as whether the company invests in employee training and wellbeing—and the levels of employee satisfaction, engagement and retention.

ISSB Standards specify information that has been identified as being decision useful to investors

Once a company has identified the sustainability-related risks and opportunities that could reasonably be expected to affect its prospects, preparers will use ISSB Standards to disclose material information related to those sustainability-related risks and opportunities.

IFRS S1: prescribes how a company prepares and reports its sustainability-related financial disclosures. It sets out general requirements for the content and presentation of those disclosures, so that the information disclosed is useful to primary users.

IFRS S2: sets out supplementary requirements that relate specifically to climate-related risks and opportunities. If a company decides that a climate-related risk or opportunity could reasonably be expected to affect its prospects, the company is required to apply IFRS S2 in preparing its climate-related disclosures.

All disclosures required by IFRS S1 and IFRS S2 are subject to an assessment of materiality.

A company is required to apply ISSB Standards together:

IFRS Sustainability Disclosure Standards (currently IFRS S1 and IFRS S2) are designed to be applied together and alongside future Standards issued by the ISSB. IFRS S1 and IFRS S2 include reporting requirements across four content areas: governance; strategy; risk management; and metrics and targets.

These core content areas are consistent with the TCFD’s recommendations.

IFRS S1 sets out overarching disclosure requirements

A company is required to apply IFRS S2 with IFRS S1. This is because IFRS S1:

- establishes the important concepts, such as the need for connected information and the scope of sustainability-related risks and opportunities to report on;

- sets out the definition of materiality and provides important guidance on the assessment of materiality to be used when providing disclosures and when applying IFRS S2;

- sets out requirements on location and timing of reporting which apply to disclosures across all ISSB Standards;

- provides guidance on reporting changes in estimates and errors;

- provides relief from disclosing commercially sensitive information about opportunities; and

- sets out the qualitative characteristics of information a company is required to disclose.

Industry specific disclosures are required

The ISSB recognises that industry-based disclosures are decision-useful for investors. Industry-based disclosures are useful because the effects of sustainability topics vary by company and industry.

Industry-specific disclosures help companies focus reporting on the business risks and opportunities that are most relevant. This focus helps to simplify and reduce the cost of reporting; it also gives investors and other providers of capital the information most relevant to their needs.

Both IFRS S1 and IFRS S2 require that industry-specific information be provided but do not stipulate the exact disclosures to be provided—that is for a company to decide. However, guidance is provided to assist companies in providing these disclosures and to facilitate the provision of more comparable, decision useful information for investors. This is discussed further in the section below.

- IFRS S1 requires a company to consider the industry-based SASB Standards for topics beyond climate to identify sustainability risks or opportunities to report to investors.

- IFRS S2 requires a company to disclose industry-specific climate-related information and provides illustrative guidance derived from SASB Standards as non-mandatory examples to support those requirements.

What are governance disclosure requirements?

A company is required to disclose information about the governance processes, controls and procedures it uses to monitor and manage sustainability-related risks and opportunities.

The climate-related governance disclosure requirements in IFRS S2 are consistent with and complement the requirements in IFRS S1.

What are strategy disclosure requirements?

A company is required to disclose information about how it manages sustainability-related risks and opportunities. This information includes:

- a description of the sustainability-related risk or opportunity;

- the current and anticipated effects of the risk or opportunity on the company’s business model and value chain;

- the effects of the risk or opportunity on the company’s strategy and decision-making;

- the current and anticipated effects of the risk or opportunity on the company’s financial position, financial performance and cash flows for the reporting period and over the short, medium and long term; and

- the resilience of the company’s strategy and its business model to those sustainability-related risks.

IFRS S2 sets out specific strategy disclosure requirements for climate-related risks and opportunities. These include requirements for a company to disclose its climate-related transition plans and to use scenario analysis to assess and disclose its resilience to climate-related changes and uncertainties.

What are risk management disclosure requirements?

A company is required to disclose information about how it identifies, assesses, prioritises and monitors sustainability-related risks.

The climate-related risk management disclosure requirements in IFRS S2 are consistent with, and complement, the requirements in IFRS S1.

What are metrics disclosure requirements?

A company is required to disclose the metrics and targets that it uses to measure performance in relation to sustainability-related risks and opportunities.

For each sustainability-related risk and opportunity that could reasonably be expected to affect the company’s prospects, a company is required to disclose:

- metrics required by an applicable ISSB Standard (for example, IFRS S2)

- metrics the company uses to measure and monitor:

- that sustainability-related risk or opportunity; and

- its performance in relation to that sustainability-related risk or opportunity, including progress towards any targets the company has set, and any targets it is required to meet by law or regulation.

When no ISSB Standard specifically applies, companies are required to consider the guidance set out in IFRS S1 to identify appropriate disclosures.

What are the requirements on climate-related metrics in IFRS S2?

IFRS S2 sets out metrics and targets disclosure requirements for climate-related risks and opportunities including:

- cross-industry metrics categories;

- industry-based metrics; and

- climate-related targets.

A company is required to disclose information relevant to these cross-industry metric categories:

- scope 1, scope 2 and scope 3 greenhouse gases*;

- climate-related transition risks;

- climate-related physical risks;

- climate-related opportunities;

- capital deployment towards climate-related risks and opportunities;

- internal carbon prices that the company uses to assess the costs of its emissions; and

- the portion of executive management remuneration linked to climate-related considerations.

*A company’s measurement of scope 3 greenhouse gas emissions is likely to include the use of estimation rather than solely comprising direct measurement. IFRS S2 provides a scope 3 measurement framework. This framework provides guidance for a company to use in preparing its scope 3 greenhouse gas emissions disclosures.

A company is required to disclose industry-based metrics associated with its business model or activities. IFRS S2 doesn’t specify particular industry-based metrics that a company must disclose. However, in determining the industry-based metrics that the company discloses, the company shall refer to and consider the applicability of the industry-based metrics associated with disclosure topics described in the Industry-based Guidance on implementing Climate-related Disclosures.

A company is required to disclose any targets set by the company, and any targets it is required to meet by law or regulation to mitigate or adapt to climate-related risks or take advantage of climate-related opportunities, including metrics used by the governance body or management to measure progress towards these targets.

Refer to IFRS S2 for further guidance on climate-related disclosure requirements.

A company that applies ISSB Standards is required to publish its sustainability-related financial disclosures:

- as part of its general purpose financial reports; and

- at the same time as its related financial statements.

It is required that a company’s sustainability-related financial disclosures cover the same reporting period as the related financial statements.

This requirement represents a change of approach for companies that previously disclosed sustainability-related financial information in a report intended for stakeholders other than investors, lenders and other creditors. The requirement also affects companies that previously published a sustainability report later than their financial statements.

When companies first apply the ISSB Standards, optional transition reliefs are available.

These include:

- companies are allowed to limit disclosures to climate-related risks and opportunities in their first year of application of IFRS S1 and IFRS S2;

- companies are allowed to publish disclosures at a later date than their general purpose financial reports, but no later than nine months after the end of the reporting period to which the disclosures apply;

- companies are not required to:

- provide disclosures about scope 3 GHG emissions;

- apply the GHG Protocol Corporate Standard to measure emissions if they are already using a different measurement approach;

- provide comparative information.

These reliefs are only available in the first annual reporting period, they are not available in subsequent reporting periods.

The application of ISSB Standards, with additional information disclosed where necessary, will result in a complete set of sustainability-related financial disclosures on all sustainability-related risks and opportunities that could reasonably be expected to affect a company’s prospects.

Use IFRS Sustainability Disclosure Standards (including disclosure topics and sources of guidance) to identify sustainability-related risks and opportunities that can reasonably be expected to affect the entity's cash flows, its access to finance or cost of capital over the short, medium or long term.

Disclose material information about each sustainability-related risk and opportunity using disclosure requirements and sources of guidance outlined within the IFRS Sustainability Disclosure Standards.

IFRS sustainability-related financial disclosures should:

- faithfully represent all sustainability-related risks and opportunities that could reasonably be expected to affect a company’s prospects;

- include material information about the sustainability-related risks and opportunities that are reasonably expected to affect the company’s prospects;

- be for the same reporting entity as related financial statements;

- enable primary users—existing and potential investors, lenders and other creditors—to understand connections between:

- various sustainability-related risks and opportunities that could reasonably be expected to affect the company’s prospects; and

- disclosures provided by the company that are:

- within its sustainability-related financial disclosures—such as connections between disclosures on governance, strategy, risk management and metrics, and targets; and

- across its sustainability-related financial disclosures and other general purpose financial reports published by the company (the financial statements).

IFRS Sustainability Disclosure Standards require a company to identify sustainability-related risks and opportunities throughout its value chain that are reasonably expected to affect its prospects.

To identify sustainability-related risks and opportunities, the company is required to exercise judgement and use all reasonable and supportable information that is available at the reporting date, without undue cost or effort.

IFRS Sustainability Disclosure Standards include specific guidance intended to assist preparers in identifying sustainability-related risks and opportunities.

What is material information?

Information about sustainability-related risks and opportunities is material if omitting, misstating or obscuring this information could reasonably be expected to influence primary users’ decisions about providing resources to a company, or to influence management’s actions.

Information about a sustainability-related risk or opportunity might be material because of the nature or magnitude of that risk or opportunity, or a combination of both, judged in relation to the company’s circumstances.

ISSB Standards specify decision-useful information for investors

After a company identifies sustainability-related risks and opportunities that could reasonably be expected to affect the company’s prospects, it is required to identify and disclose material information related to those sustainability-related risks and opportunities. This includes information about a company’s governance, strategy and risk management in relation to those risks and opportunities, and related metrics and targets. The particular information that is material and thus must be disclosed will depend on a company’s facts and circumstances and may vary over time.

IFRS S1: references sources of guidance that might be useful to companies in disclosing material information about each sustainability-related risk and opportunity identified. The sources of guidance specify information, including metrics, that might be relevant to a particular sustainability-related risk or opportunity, to a particular industry or to specified circumstances.

IFRS S2: requires that a company discloses industry-based metrics associated with particular business models, activities or other common features that characterise participation in an industry. A company is required, in preparing disclosures to meet this requirement, to refer to and consider the applicability of industry-based metrics associated with disclosure topics. These are defined in the Industry-based Guidance on implementing Climate-related Disclosures.

A company is required to apply judgement to assess whether information prescribed in the applicable ISSB Standards and sources of guidance is material—either individually or in combination with other information.

Making materiality judgements

- Is the information, identified either individually or in combination with other information, material in the context of the company’s sustainability-related financial disclosures taken as a whole?

- Have you considered both quantitative and qualitative factors?

- Have you considered the potential effect of future events on the amount, timing and uncertainty of the company’s future cash flows over the short, medium and long term?

- Have you considered the range of possible outcomes and the likelihood of the possible outcomes within that range?

Avoid obscuring material information

IFRS S1 permits a company to present additional information disclosed to meet other requirements, such as specific jurisdictional requirements. But the company is prohibited from obscuring material information with that additional information.

Examples of circumstances that might result in material information being obscured include those where:

- material information is not clearly distinguished from additional information that is not material;

- material information is disclosed in the sustainability-related financial disclosures, but the language used is vague or unclear;

- material information about a sustainability-related risk or opportunity is scattered throughout the sustainability-related financial disclosures;

- items of information that are dissimilar are inappropriately aggregated;

- items of information that are similar are inappropriately disaggregated; and

- the understandability of the sustainability-related financial disclosures is reduced because of material information being hidden by immaterial information to the extent that a primary user is unable to determine what information is material.

Questions to consider when assessing material information to disclose

- Does the information provide a complete, neutral and accurate depiction of those sustainability-related risks and opportunities?

- Is information disclosed comparable, verifiable, timely and understandable?

- Does the information disclosed cover the same reporting period as the related financial statements?

- Is the information presented in a manner that enables users to understand connections:

- between various sustainability-related risks and opportunities that could reasonably be expected to affect the company’s prospects;

- between disclosures on governance, strategy, risk management and metrics and targets; and

- across its sustainability-related financial disclosures and other general purpose financial reports published by the company (eg financial statements).

- Are data and assumptions used in preparing the sustainability-related financial disclosures consistent with the corresponding data and assumptions used in preparing the related financial statements?

- Would the omission, misstatement or obscuring of information about critical dependencies on resources and relationships, or significant external environment influences, reasonably be expected to influence primary users’ decisions and/or compromise their common information needs?

How can I learn more about IFRS Sustainability Disclosure Standards?

- Access IFRS Sustainability Disclosure Standards and accompanying guidance using the IFRS Sustainability Standards Navigator. All IFRS Sustainability Standards Navigator content is available to registered web users at no cost.

- Access Supporting materials for IFRS Sustainability Disclosure Standards.

- Review other ISSB Frequently Asked Questions.