The IFRS for SMEs Accounting Standard Update is a staff summary of news, events and other information about the IFRS for SMEs® Accounting Standard and related SME activities. The staff summary has not been reviewed by the International Accounting Standards Board (IASB).

This edition of the IFRS for SMEs Accounting Standard Update includes:

- an overview of outreach activities on the Exposure Draft Third edition of the IFRS for SMEs Accounting Standard (the Exposure Draft);

- an invitation to participate in fieldwork to test the proposed requirements in the Exposure Draft for Section 23 Revenue from Contracts with Customers; and

- an invitation to apply or nominate candidates for membership of the SME Implementation Group (SMEIG).

Overview of outreach activities on the Exposure Draft

The IASB is undertaking its second comprehensive review of the IFRS for SMEs Accounting Standard.

On 8 September 2022, the IASB published the Exposure Draft as part of the second comprehensive review. The comment period on the Exposure Draft closed on 7 March 2023.

Outreach events

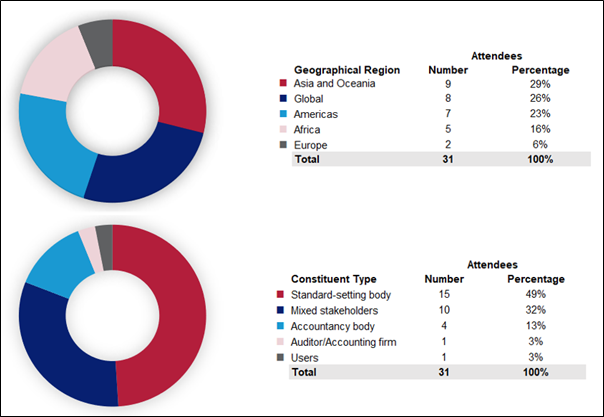

During the comment period, the IASB members and staff met remotely and in person with stakeholders in 31 outreach events globally, including meetings, discussion forums, conferences, seminars and roundtables.

Figure 1 illustrates the geographical distribution of attendees at outreach events. Events were relatively evenly distributed across geographical regions, with the highest number of events in Asia/Oceania and the Americas, or were global events. The largest number of attendees came from accountancy bodies and standard-setting bodies.

Figure 1—Outreach events by region and constituent type

Comment letters

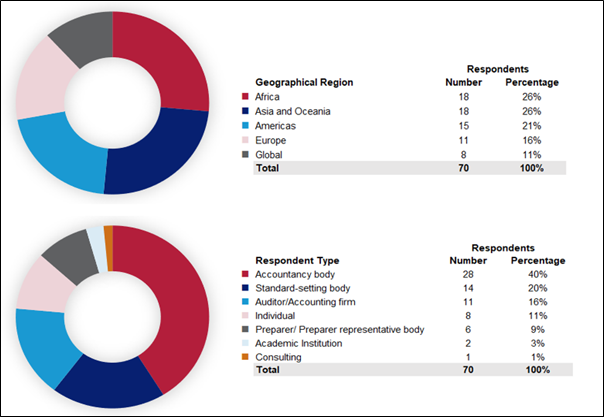

As of 14 March 2023, the IASB received 70 comment letters on the Exposure Draft.

The comment letter data followed a similar pattern to the outreach events, with a geographical distribution led by Africa, Asia/Oceania and the Americas and respondent types led by accountancy bodies and standard-setting bodies.

Figure 2—Comment letters by region and respondent type

Exposure Draft and comment letter page views

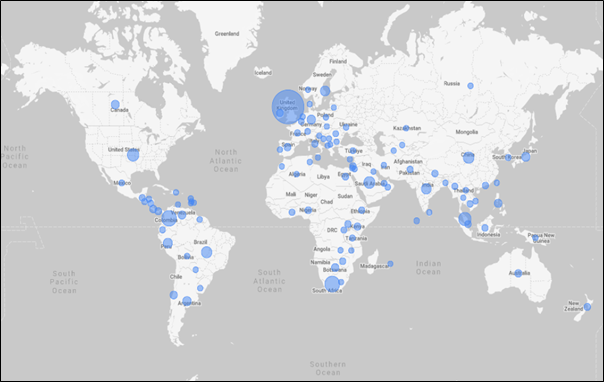

The Exposure Draft and comment letter webpage has so far been viewed by more than 7,800 stakeholders globally.

Page views were led by Asia-Oceania, the Americas and Europe.

Figure 3—Map of Exposure Draft and comment letter page views

Next steps

During the next phase of the review, the IASB will analyse and deliberate the feedback from the outreach events and comment letters.

The IASB is also undertaking fieldwork on the proposals in Section 23 Revenue from Contracts with Customers of the Exposure Draft, see below.

Please visit the project page for other updates and more information about the project.

Invitation to participate in fieldwork to test the proposed requirements in the Exposure Draft—Section 23 Revenue from Contracts with Customers

The Exposure Draft includes a proposal to revise Section 23 Revenue to align it with the principles and language used in IFRS 15 Revenue from Contracts with Customers, with simplifications.

Accounting practitioners who are involved in the preparation of SMEs’ financial statements are invited to take part in fieldwork to test the proposed requirements.

The field test is being conducted to understand whether preparers can make the judgements necessary to apply the proposed revised Section 23. The results of the field test will be considered by the IASB as part of its redeliberation process.

Participants will be asked to:

- fill out a questionnaire; and

- discuss their response to the questionnaire with the SME project team.

The aim is for the questionnaires and follow-up calls with participants to be completed by 30 April 2023.

Taking part in the field test offers practitioners an opportunity to learn more about the IASB’s proposals and the likely practical effects of the proposed requirements.

Participants are not required to have any prior knowledge of IFRS 15 and will not be asked to prepare financial statements or disclosures in accordance with the proposed requirements.

Practitioners who would like to participate in the fieldwork and receive a questionnaire should send an email to sme@ifrs.org outlining their interest to the project team. The questionnaire is available in Spanish and English.

Invitation for applications and nominations for membership of the SMEIG

The Trustees of the IFRS Foundation (Trustees) invite applications and nominations of candidates for membership of the SME Implementation Group (SMEIG). The mission of the SMEIG is to support the international adoption, implementation and application of the IFRS for SMEs Accounting Standard.

A key responsibility of the SMEIG is making recommendations to the IASB on proposed amendments to the IFRS for SMEs Accounting Standard during this second comprehensive review.

SMEIG members are selected for their knowledge of and experience in financial reporting by small and medium-sized entities and, preferably, for their knowledge of and direct experience with the IFRS for SMEs Accounting Standard. Candidates must be proficient in spoken and written English. All SMEIG members serve on a voluntary, unpaid basis.

Applications and nominations should be submitted in English and will be considered if they are received at sme@ifrs.org by 6 April 2023. Further information on the criteria for membership and the Terms of Reference and Operating Procedures for the SMEIG is available on our website.